CLICK HERE FOR YOUR FREE MEDWAY PROPERTY NEWSLETTER

Could the high levels of mortgages that Medway people take out cause another property crash?

Many Medway homeowners and landlords have been contacting me recently and asking what will happen to the Medway (and the UK) property market? More specifically, will we have a repeat of the 2008/9 Credit Crunch property crash?

High mortgage payments were one of the critical catalysts to Medway house prices dropping by between 16% and 19% (depending on the type of property) in just over one year in Medway.

To answer that question, let me look at the mortgage numbers locally to see where we stand in the Medway area.

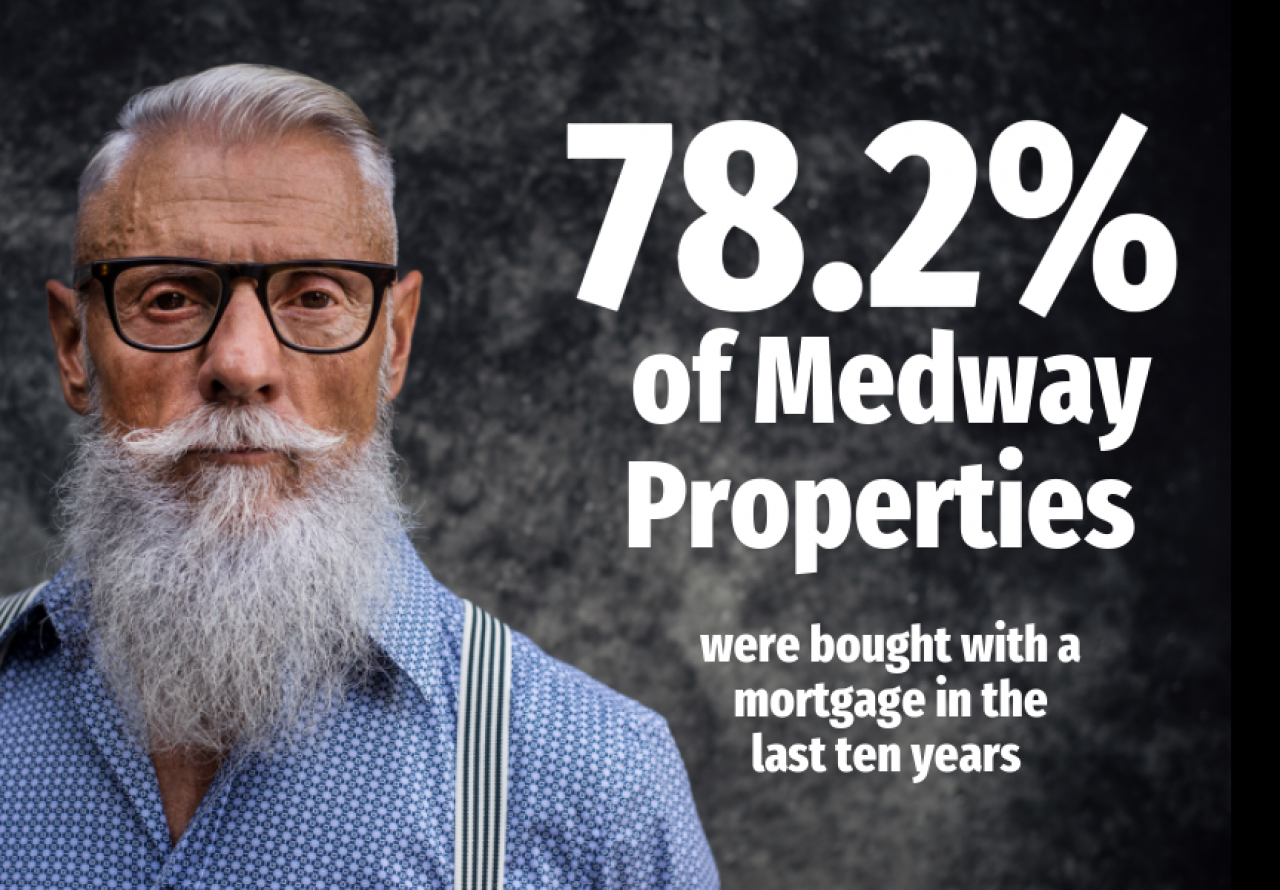

32,426 of the 41,454 property sales in the last decade in Medway were made with a mortgage

78.2% of our local authority area house purchases have been made with a mortgage (meaning 21.8% are made with 100% cash).

Interesting, when compared with the national average of 67.4% of house purchases with a mortgage over the last decade.

However, what is thought-provoking is the number of house purchasers buying with a mortgage has steadily been increasing over the last decade.

Between 2012 and 2017, the percentage of people buying with a mortgage was 76.0%, yet over the last five years in Medway, that has risen to 82.2%

Initially, this doesn't sound good. Yet, as always with my articles on the Medway property market, the devil is in the detail.

The issue is that most people need a mortgage to buy their home.

However, it’s not the amount of mortgage that is the issue, more the level of monthly payments. So, if you fix your mortgage rate, then your payments are fixed (a good idea especially as interest rates are on the rise).

In the last quarter, just under nineteen out of twenty (94.35%) of new borrowers that took out a mortgage had a fixed-rate mortgage at an average interest rate of 1.84%

That’s good news for recent buyers as most of their payments won’t rise even though Bank of England interest rates have risen over the last few months. Yet it’s essential to see what existing homeowners with mortgages have done with their mortgage rates (i.e. fixed or not) as they form the bulk of the property market.

This is because in 2008/9 (the last crash), many people were unable to afford their high monthly mortgage payments when they were made redundant because interest rates were much higher. This meant many Medway homeowners ‘dumped’ their houses onto the market, all in one go in 2008, because they couldn’t afford their high mortgage payments.

Also, the banks could not lend money for mortgages as easily because of the Credit Crunch, meaning fewer people could get a mortgage, so the demand for Medway houses dropped as well.

In a nutshell, the number of Medway properties on the market almost doubled overnight in 2008, yet demand plummeted as mortgages were hard to come by. High supply and low demand meant Medway house prices nosedived in 2008/9

Going into the Credit Crunch, one in six (60.4%) homeowners with a mortgage had a fixed rate at an average rate of 5.76%. By 2013, this had dropped to one in three people (33.29%) having a fixed-rate mortgage at an average of 3.34%.

Yet today, just under 17 out of 20 homeowners with a mortgage have a fixed rate at an average of 1.97%

Whilst the country might owe collectively £1,630.5 billion in mortgages, irrespective of increasing rates, most homeowners have protected themselves with a low fixed interest rate.

Also, the overall ratio of mortgage debt in the UK, compared to the value of the homes the mortgages are lent on, is also low compared to the year before the last property crash. This ratio is called the Loan to Value ratio (LTV). The higher the LTV, the less equity the homeowner has in the property.

In 2007 (the year before the crash), only 49.4% of people had a mortgage less than 75% of the house's value (i.e. they had an LTV of less than 75%). Today that stands at 60.9%, which means more people have more equity in their property.

Another thought on why the country is in a better position is only 4.22% of mortgages have a 90% or higher LTV (compared to 16.28% just before the crash in 2007).

1 in 6 people were vulnerable to negative equity in the last property crash, whilst today that would only be 1 in 25.

This means if we do have another property market correction for any other reason ... the number of people in negative equity will be much smaller, so it won't affect the property market as much.

So, in conclusion, as we have fewer people with high LTV mortgages and fixed rates that are a third of what they were in the Credit Crunch, we are, as a country, in a better position to weather any storm.

If you would like any advice or opinion on the Medway property market, be it buying or selling or anything to do with investing in the Medway buy-to-let property market, don't hesitate to drop me a line.

One place for more information is my Medway Property Market blog. If you are a landlord or thinking of becoming one for the first time, and you want to read more articles like this about the Medway property market together with regular postings on what I consider the best buy to let deals in Medway, then it is well worth reading. You can also email me at spencer@docksidekent.com

If you are in the area feel free to pop into the office which is based at Station Road, Strood, Kent, ME2 4WQ

Don’t forget to visit the links below to view back dated deals and Medway Property News.

Click Here For Your Free Medway Property Valuation

Free Valuation - https://docksidekent.com/value-my-property

Blog – http://www.medwaypropertyblog.com/

Facebook – https://www.facebook.com/DocksideP/

Website – http://www.docksidekent.com/

By

By

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link