By

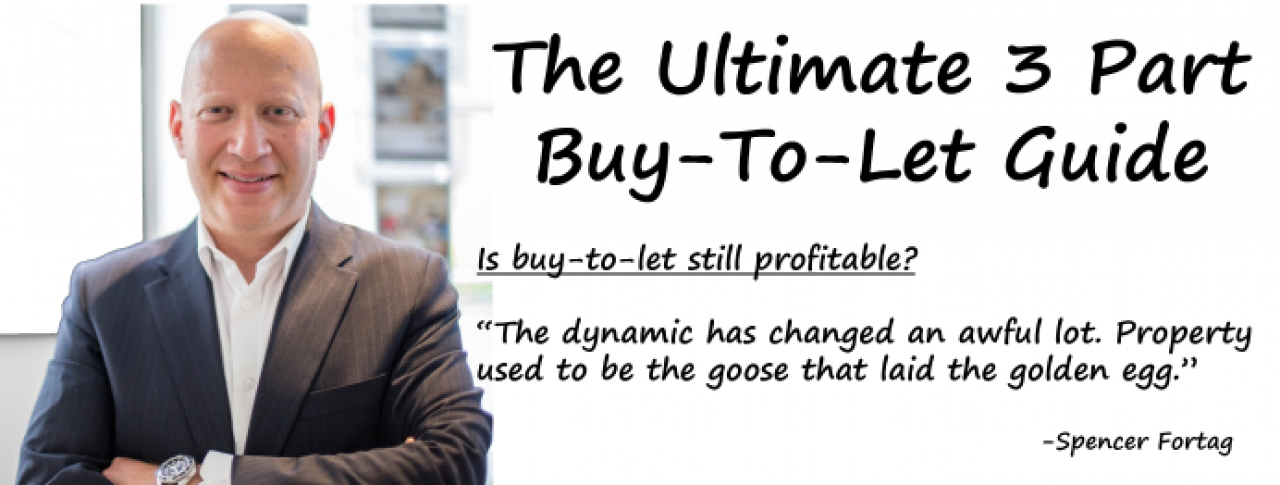

By Thanks to The Telegraph for asking me my thoughts on the buy to let market:

The ultimate buy-to-let practical guide: how to maximise your profits.

Do you want to invest in buy-to-let but don't know where to start? In this weekly four-part series, we break it down, looking at the money you need to spend, how to strategies your investment, how to manage agents and tenants, and how to maintain a property

Tax changes, a global pandemic and rising unemployment mean that the appeal of investing in buy-to-let has diminished in recent years.

But so has the viability of other asset classes: interest rates are at record lows and the stock market is volatile.

Meanwhile, the property market is booming and rents are rising almost everywhere outside London.

In this four-part series, we’re looking at the practical side of buy-to-let. First up: is the dream of being a landlord still financially viable?

Is buy-to-let still profitable?

Spencer Fortag, of Dockside Property Services estate agents, and a portfolio landlord, said: “The dynamic has changed an awful lot. Property used to be the goose that laid the golden egg.”

The introduction of a 3pc stamp duty surcharge on additional properties in 2016 hit the sector hard, followed by the reduction in tax relief on buy-to-let mortgages in 2017.

Before then, landlords could deduct all of their mortgage interest costs from their tax bill. Since April 2017, that relief has been tapered. Now, landlords instead receive a tax credit, worth 20pc of their mortgage interest costs. This has hit profits significantly.

Michael Martin, of Seven Investment Management, said if the yield on a long-term let is low, the tax costs on top mean “you’re basically paying someone to live in your house”.

But there are still ways to get significant returns on investment. Much depends on where you invest, with a focus on areas with high yields and demand; the rental market outside the capital is strong. Max Armstrong, of North East Property Investment, a buy-to-let specialist, said: “We manage 330 properties, and only three of them are currently available to rent at the moment.”

First-timers should start with a minimum of £50,000, said Mr Armstrong. This will cover the 25pc deposits and refurbishment costs for two properties in the North East. Together, they will bring in a rental income of £750 per month, he said.

“Then after six months you can refinance, put the money in another property and bring your income up to £1,000 per month, said Mr Armstrong. “You will get a return on your capital of 20pc without a doubt.”

When and what is best to buy?

The pandemic has brought falling rents in London and has accelerated the number of investors moving North to chase higher yields. As a result of this higher demand, people are paying 10pc more than normal at the lower end of the market, said Mr Armstrong.

“There is certainly a little bubble at the moment, in the North East particularly,” he added. “If you’re buying for capital growth, now is not the time to invest; sit it out until the end of March 2021.”

“We’re telling some clients to hold on a couple of months,” said Mr Fortag. The furlough scheme has just ended and many anticipate widespread unemployment – which could put downward pressure on both rents and house prices.

Choosing where to invest is a trade-off between capital growth and yields, what Mr Fortag calls “the buy-to-let see-saw”.

“The ideal property is where that is fairly balanced,” he said. Cheaper areas offer higher yields than expensive areas but typically less capital growth – and vice versa.

“Don’t buy what you like,” added Mr Fortag “Speak to five or six local lettings agents and buy what is most in demand with renters.” In the wake of the pandemic, tenants are looking for larger properties with outdoor space and good broadband, he added. “Look for bigger, freehold homes in the suburbs.”

How to buy at auction and get a bargain

The best buy-to-let deals can often be found on the auction market. The buying process is quick: there is typically a three week period between a catalogue being released and a sale.

When the hammer goes down on a property, that is the exchange of contract. The buyer has to pay a 10pc deposit immediately and must complete within 28 days.

Sellers are there for the speed and in exchange for the surety of a sale, they typically take a price hit. Andrew Brown, of Strettons auction house, said: “The rule of thumb is that homes will achieve 80pc of the private treaty price.”

Buying at auction is almost impossible for anyone in a chain. There is little competition from owner occupiers, and 95pc of buyers at auctions are property professionals, such as investors, developers and property traders, said Mr Brown.

There is also an added degree of risk. Sellers produce a legal pack ahead of the sale which normally includes local authority searches and title plans, but rarely a survey. Buyers can pay for these before a sale, but there is no guarantee that they will be the highest bidder on the property, said Mr Brown.

If they choose to buy without a survey, there is no option to renegotiate the price after the auction.

The costs you need to factor in

To buy a £60,000 property in the North of England, you will need £15,000 for a 25pc deposit (the standard for buy-to-let mortgages). Factor in an extra £10,000 to cover things like stamp duty (£1,800 at 3pc – this is unchanged by the stamp duty holiday as the price is already below the standard nil-rate band of £125,000), legal fees (about £1,000), and refurbishment costs, said Mr Fortag.

He recommends getting a fixed-rate mortgage. “It will cost you £100 or so extra but you will have financial stability,” he said.

Budget £2,000 per year per property for repairs and maintenance. Mr Fortag recommends paying rent guarantee insurance, which typically costs 4pc of the year’s rent. If it is not possible to get this, keep a pot of three months’ worth of rent to cover yourself for void periods.

The crucial question when investing in property, particularly in a period of extreme uncertainty, is to ask “how are you going to get out in a worst case scenario?” Mr Martin said.

Feel free to contact me with any property questions you may have or for any advice you may need. Email me via:spencer@docksidekent.com

Did you know you can get an rental and sales valuation on your property, online and in under 58 seconds? Just enter your postcode using the link Below:

Click Here For Your Free Medway Property Valuation

You can also keep up to date with all the Medway property news by signing up to my Medway Property News Letter on the link below

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link